this post was submitted on 07 Aug 2024

920 points (98.9% liked)

People Twitter

7499 readers

620 users here now

People tweeting stuff. We allow tweets from anyone.

RULES:

- Mark NSFW content.

- No doxxing people.

- Must be a pic of the tweet or similar. No direct links to the tweet.

- No bullying or international politcs

- Be excellent to each other.

- Provide an archived link to the tweet (or similar) being shown if it's a major figure or a politician.

founded 2 years ago

MODERATORS

you are viewing a single comment's thread

view the rest of the comments

view the rest of the comments

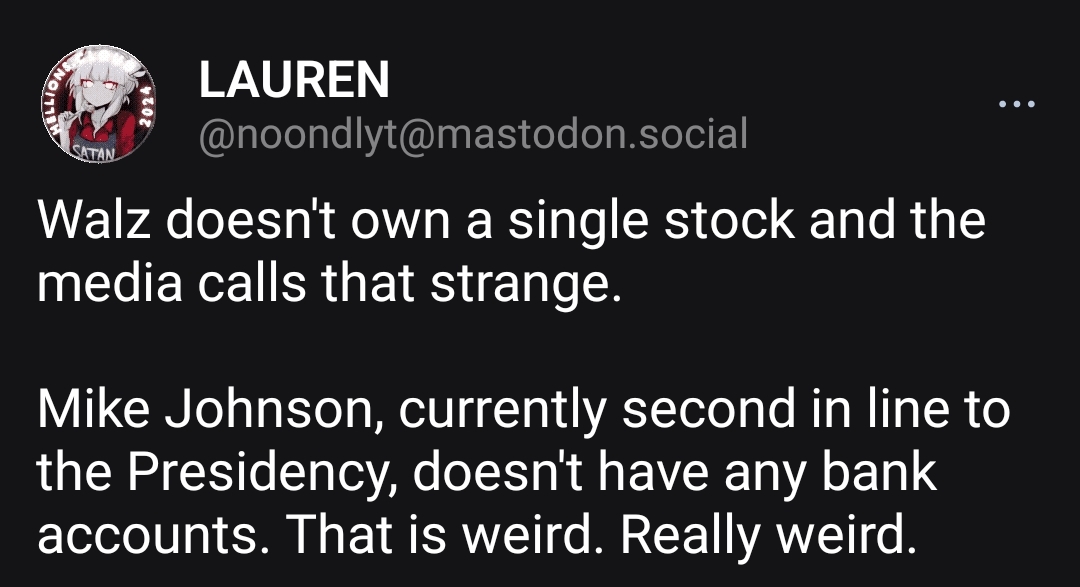

According to FDIC, about 4.5% of US households do not have a bank account of any kind, but that number is much higher when you only include low income households. Some choose not to have an account, some are denied accounts by banks for various reasons.

https://www.fdic.gov/analysis/household-survey/index.html

Also, most banks only offer free checking accounts with direct deposit or a minimum balance. I don't know if this is still the case, but I worked for a payroll processor many years ago and, at that time, many small businesses chose not to offer direct deposit to their employees. Paying bank fees is very difficult for low income households.

One of the options the company I worked for had was to offer refillable debit cards to employees that their paychecks would be deposited to. This gave them the basic features of a bank without needing to create their own account.

I had not heard of this before. So who owns the account? Can they go to the bank website and check their balance and transfer money? Can they pay bills online? Withdraw cash from an atm?

If so, that has pretty much all the functionality of a checking account. I suppose minus the actual check writing. Are they worried low income people will do check fraud? Or maybe just overdraw with checks?

It's been a long time since I worked in that space, but I think it is basically like a reloadable prepaid card you can get from visa or mastercard. I would assume there actually is a bank behind it, but the account is essentially being sponsored by someone else and there is less risk for the bank because you can't write a bad check or overdraw the account. That makes it potentially useful if the reason you didn't get an account is because the banks refused you or you couldn't afford the fees. For people who are just anti-bank or worried about financial privacy, they would still want to go cash only.

On a side note, reloadable cards can also be useful if you have friends or relatives that you want to help out now and then, especially if they are not local and maybe make poor decisions. It's cheaper than Western Union or a money order, more secure than mailing cash, and no risk of them having access to your bank account number from sending a check.

I briefly worked for a place that paid to a pre-paid Visa card like you're saying. They basically gave you the card when you started and you did all the activation. It was a temp agency so it made it more convenient when it came to getting paid per diem or for short term work. The business paid the agency, the agency paid you. At the time it didn't seem too sketchy (20+ years ago) but I'd be pretty cautious about doing something like that now.